Should you be investing in Canadian tech name Lightspeed POS (Lightspeed POS Stock Quote, Chart, News TSX:LSPD)? That depends on how risky you want to be with your money.

If high-growth potential is your thing, go for LSPD, says portfolio manager Jason Mann of EdgeHill Partners, who says the stock is on a roll at the moment. But if profitability and steady returns are more

up your alley, Lightspeed is probably the wrong bet, he said.

“This is another stock that we would put in that growth bucket…growth at any price,” said Mann, chief investment officer at EdgeHill, in conversation with BNN Bloomberg last Thursday.

“If we look at it on our metrics of valuation and trend, its trend has certainly rebounded sharply. But it scores pretty poorly for us on valuation,” Mann says. “No earnings to speak of —it actually missed on the last quarter— negative return on equity. It’s a volatile stock, as well.”

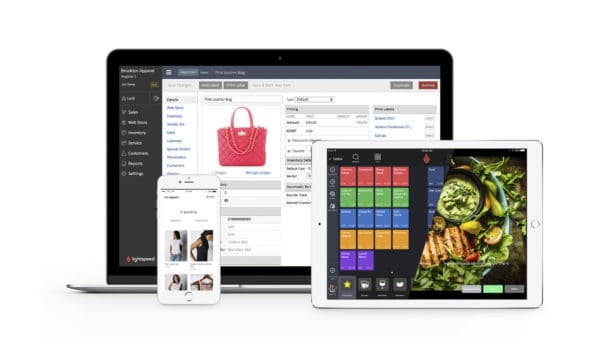

Montreal-based Lightspeed, which has a point-of-sale and analytics platform focused on the small and medium-sized business market, came out with a flashy IPO last year, the largest tech public listing in the Canadian market in almost a decade.

And while the stock saw huge gains in the first 12 months of its existence, LSPD fell hard during the market pullback of late February and March of this year, with speculation being that its restaurant and retail customers —both hard hit by COVID-19— would be scaling back their business with Lightspeed.

Yet last month the company posted surprisingly strong results for the quarter ended March 31, showing revenue up 70 per cent year-over-year to $36.3 million and a loss of $18.6 million versus a loss of $96.1 million a year prior. (All figures in US dollars except where noted otherwise.)

Lightspeed even managed to grow its customer base substantially over the quarter (its fiscal fourth 2020), ending with 76,500 customers compared to 49,000 a year earlier, while gross profit climbed to 58 per cent to $77.4 million on a gross margin of 63 per cent. Adjusted EBITDA for the Q4 climbed to a negative $6.2 million compared to negative $4.1 million a year earlier.

Those numbers lifted the stock to the C$33.00 range where it has languished over the past two weeks, but the gains for April and May were huge (almost 73 per cent for the two months), making it a stock with lots of momentum behind it, Mann said.

“Clearly it’s got good trend, so on a pure trend basis I can understand why people own it and on a growth basis I understand why people own it,” Mann said. “But it would be something we would avoid only because it doesn’t have the valuation underpinning. It’s not for us.”

Last month, Lightspeed announced a collaboration with the province of Quebec’s retail business association, Le Conseil québécois du commerce de détail (CQCD) to give retailers in Quebec assistance through the COVID-19 crisis by offering LSPD’s point-of-sale and omnichannel services at a discount.

“We understand that when retailers have the capability to meet their customers where they are, 24 hours a day and seven days a week, that it puts these businesses at a huge advantage —especially in the current climate,” said Lightspeed president JP Chauvet in a May 20 press release.

“Our collaboration with the CQCD provides retailers with meaningful advice and access to digital resources that are integral to how they continue doing business during this time,” Chauvet said.

About The Author /

Cantech Letter founder and editor Nick Waddell has lived in five Canadian provinces and is proud of his country's often overlooked contributions to the world of science and technology. Waddell takes a regular shift on the Canadian media circuit, making appearances on CTV, CBC and BNN, and contributing to publications such as Canadian Business and Business Insider.

Leave a Reply

You must be logged in to post a comment.

RELATED POSTS

Share

Share Tweet

Tweet Share

ShareTRENDING

All Trending →

WonderFi Technologies keeps $0.65 target at Haywood

February 20, 2025

CGI Group is a “premium operator”, National Bank says

January 30, 2025

Real Matters is an undervalued stock, ATB says

January 29, 2025

EA has price target slashed at Roth

January 23, 2025

Comment